money

money Some American homeowners are making a big retirement mistake, survey finds

Some Americans are pinning their retirement hopes on their homes, betting that housing appreciation will continue and compensate for their lack of savings.

But experts warn that adults shouldn’t bank on houses as their only retirement investment – even if real estate appreciation continues.

One in 4 U.S. homeowners plan to use their home to fund their retirement, according to a recent survey from Unison, a home co-investing firm. Of those, 1 in 6 said their home represents half or more of their retirement nest egg.

“If someone thinks their home is going to fund 100% of retirement, that’s a little scary, but I’m not surprised,” said James Ciprich, advisor at RegentAtlantic, a financial planning firm. “We have a retirement savings crisis.”

Rosy outlook on home values

Home values in the U.S. have increased by almost 59% since bottoming out in February 2012, according to the most recent estimates from the S&P/Case-Shiller index. That’s helping to convince 70% of American homeowners that their home will be worth more by the time they retire, according to the survey.

More than a third estimate their home’s value will increase by 10% or more; a quarter expect at least a 25% gain; and 1 in 12 believe their home’s worth will jump 50% or more.

“Home prices are increasing faster than wages,” said Rayan Rafay, chief operating and financial officer at Unison. “And therefore people look to wealth in their homes as a result.”

But home prices don’t always go up.

From mid-2006 to the beginning of 2012, housing values dropped 27% nationally, according to Case-Shiller, with many markets experiencing steeper losses. That could spell trouble for those relying on their homes for retirement. Almost 2 in 5 say a similar 25% drop in home values would delay their retirement.

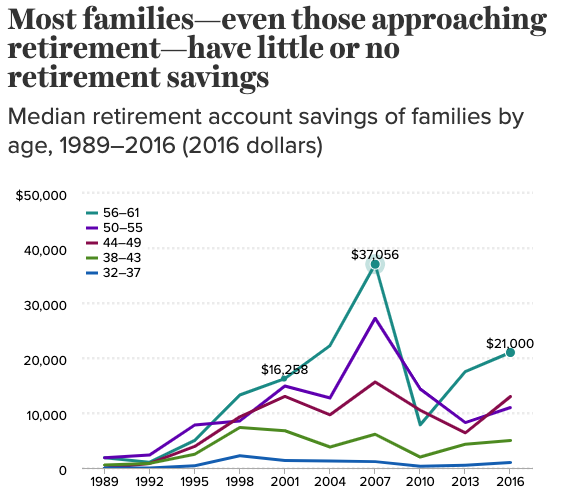

Meager retirement savings

Another reason Americans are depending on their homes for their golden years is because they lack savings in their retirement accounts.

According to a study by the Economic Policy Institute, the mean retirement account amount of workers in their 50s has stagnated over the last decade, compared with previous generations. The median retirement account savings in 2016 hovered just around $21,000.

“The trends are still troubling on how ill-prepared people are for [retirement],” said Rich Ramassini, senior vice president of sales strategy and performance at PNC. “People struggle to manage multiple financial priorities, such as student loan debt.”

How your home fits into retirement

It’s important to diversify your retirement fund rather than relying solely on your home.

Doing so can create a problem because “your home is not immediately liquid,” said Dan Slagle, founding partner at Fyooz Financial Planning. “The proceeds may be locked up for months depending on the state of the housing market.”

Your home should not be more than 20% to 30% of your total net worth, Slagle said, with the rest coming from your savings and investments.

"People purchase their home with the idea that it is a great investment vehicle," he said. "A home should not be purchased solely because it is likely to appreciate in value."

Dhara is a writer for Yahoo Finance. Follow her on Twitter @dsinghx.

Read more:

Gen Z more than doubles its presence in housing market, study finds

States where home prices increased the most and the least in 2019

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.