money

money Half of Americans took from retirement savings or plan to amid pandemic, survey finds

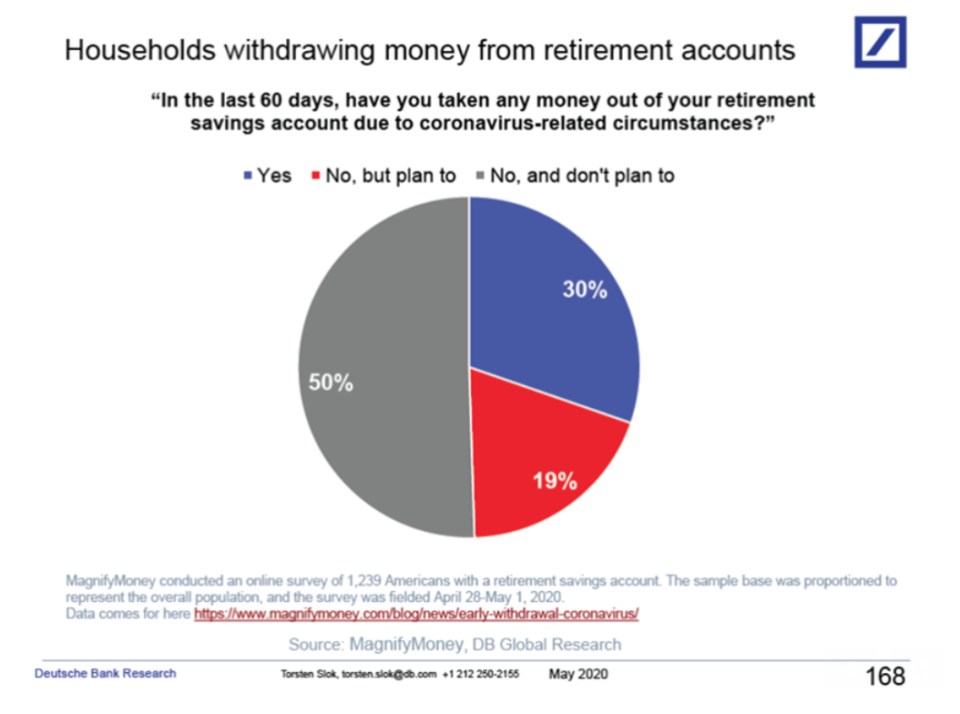

Nearly half of Americans dipped into their retirement accounts recently or are considering the move, according to a new survey.

Three in 10 Americans withdrew $6,757.20 on average from their retirement accounts in the last two months, according to an online survey of 1,239 Americans with a retirement savings from personal finance site Magnify Money. Another 2 in 5 plan to do so soon, the survey found.

The findings come as jobless claims surpassed 36 million, leading Americans to dig into their savings to stay afloat. Recent provisions from the CARES Act also eased penalties for early withdrawals up to $100,000 due to coronavirus related hardships, making the move less burdensome.

“The preparedness was quite poor for the household sector going into the virus,” said Torsten Slok, chief economist at Deutsche Bank. “So, it’s not surprising that half the population has or is thinking about planning to withdraw from retirement accounts.”

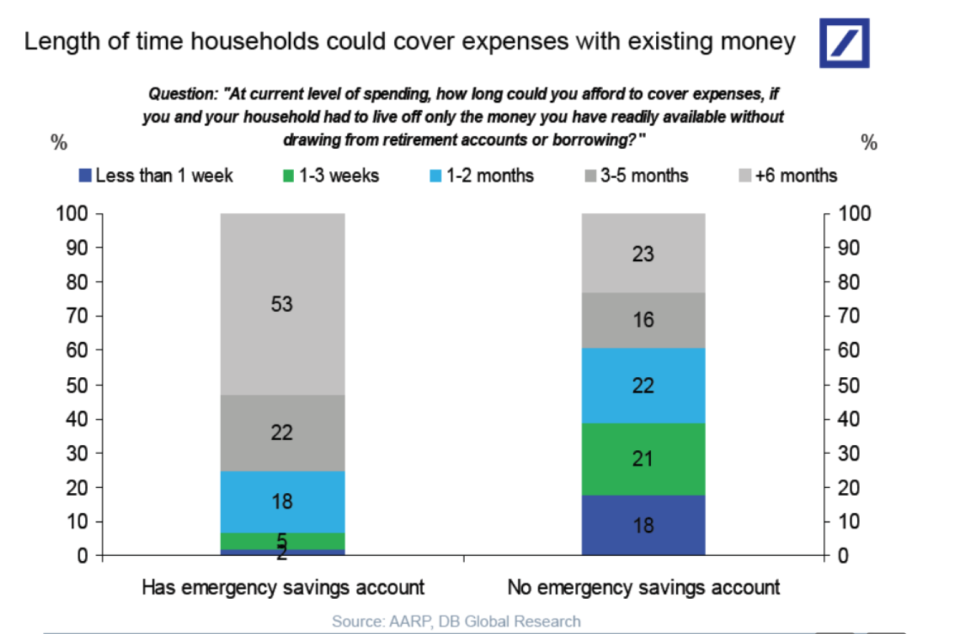

Slok referenced an earlier study that showed 61% of Americans didn’t have emergency savings or would only be able to survive two months or less from their savings.

While Slok believes jobless claims will grow at a slower rate going forward, the lingering effects may force more people to pull from their retirement accounts in upcoming weeks.

“We are worried that more people will be laid off as long as the economy is shutdown and there is no demand for services and no revenue,” Slok said.

As a rule of thumb, many financial advisors recommend clients have at the minimum six months of an emergency cushion, so they don’t have to resort to raiding their retirement savings.

“My clients are not allowed to even consider investing until they have an emergency fund set up that will cover three to six months of fixed expenses as couples or six to 12 months for a single individual,” said Dana Menard of Twin Cities Wealth Strategies.

Withdrawing from retirement savings accounts can also have serious repercussions for the future.

“You should only take money from retirement funds in extreme circumstances, such as losing your income and completely exhausting your cash reserves,” said Aaron Clarke, an advisor at Halpern Financial. “If this is the case, then of course, you should not suffer in the interim until your employment or financial situation changes.”

But Clark pointed out that if bankruptcy is an option you’re considering, you should leave the funds in your 401(k) plan alone.

“Your 401(k) assets are protected from creditors under ERISA laws. Whether IRAs are protected from creditors varies by state,” Clark said.

Dhara is a reporter Yahoo Money and Cashay. Follow her on Twitter at @Dsinghx.

Read more:

Expert: New retirees ‘are going to have to adjust their expectations’

'Fundraise for the most vulnerable': GoFundMe campaigns fill gaps before government aid kicks in

Coronavirus cash crunch leading to more Americans withdrawing from 401K accounts

Read the latest financial and business news from Yahoo Finance and Yahoo Money

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.