money

money 'Don't get your hopes up' about $30/hour average wages, economists warn

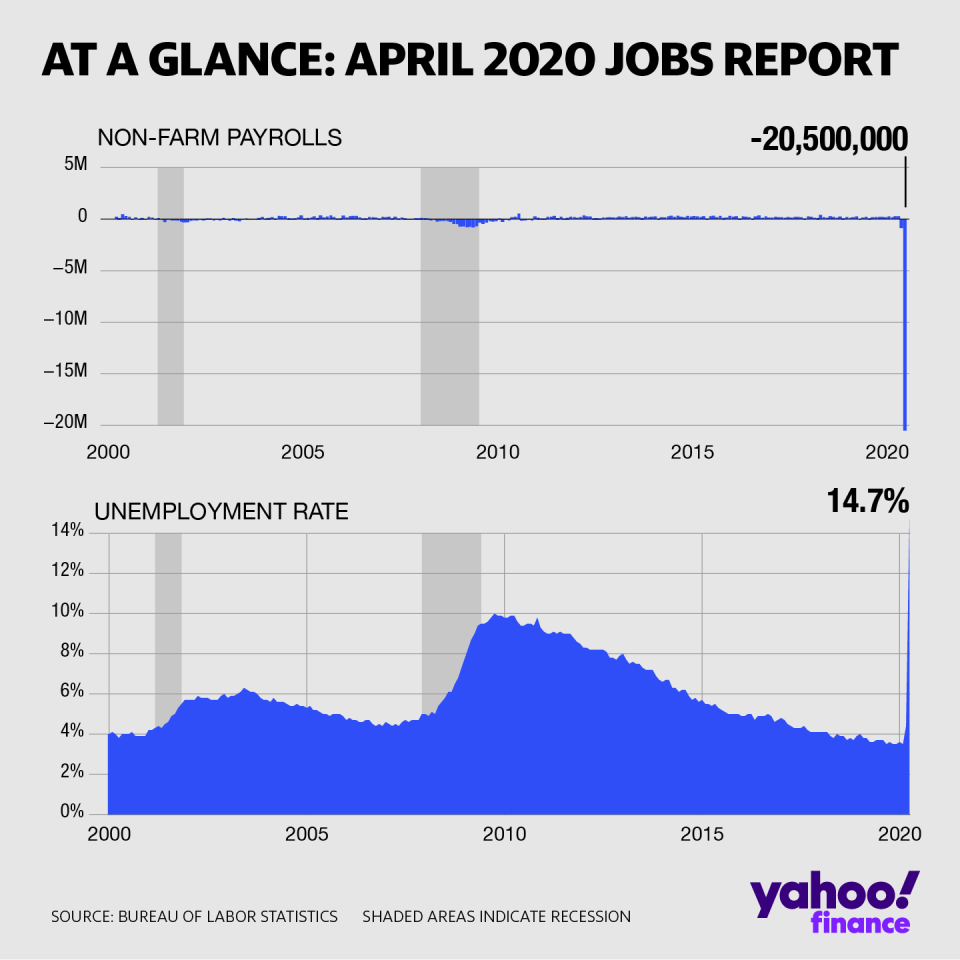

The April jobs numbers are in, providing new data on the catastrophic economic damage caused by the coronavirus crisis. Though slightly better than expectations, the preliminary numbers showed an unprecedented 20.5 million payrolls lost during April.

The Bureau of Labor Statistics’ unemployment rate was 14.7% in April, the highest since the late 1940s. The BLS even said that due to survey errors, the rate is likely five percentage points higher, bringing it to 20%.

Two bits of good news were tucked into the release: a high number of temporary layoffs, which may mean that those jobs could come back after the COVID crisis lets up (though they could become permanent), and the fact that wages grew.

However, economists say this is very misleading.

The hourly earnings figure showed a huge 4.7% increase from March to April, bringing average hourly earnings to $30.01, an increase of 7.9% compared to last year. This is really high. February’s numbers, for instance, were flat.

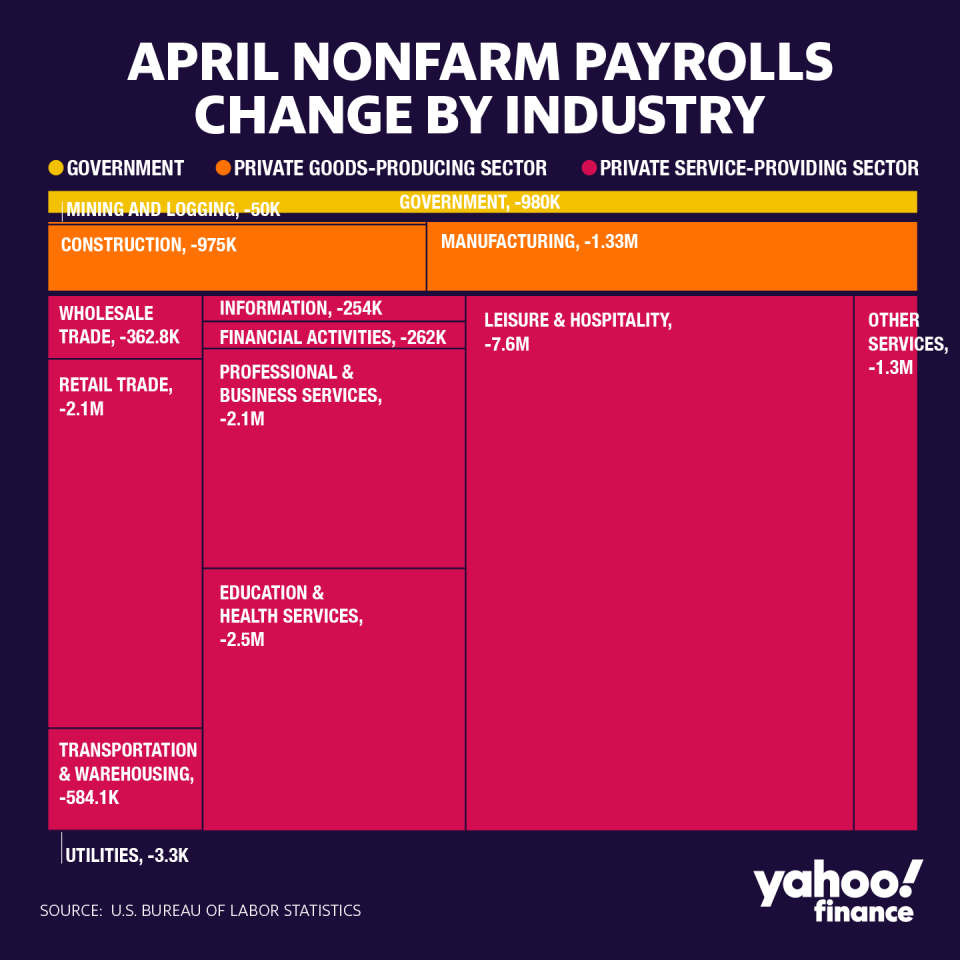

On one level, it looks like there was finally wage growth. But those numbers aren’t higher because wages were actually better – they’re a result of lower-income workers losing their jobs. When those lower-paying jobs aren’t in the calculations, average wages skew upwards.

“Wages shot up, but don't get your hopes up, it's because lower-paid workers dropped out of the equation,” Chris Rupkey, Mitsubishi UFJ Financial Group’s chief economist, wrote in a note Friday morning.

As Pantheon’s chief economist Ian Shepherdson put it, “The leap in hourly earnings is a technicality.”

“The data are just a crude average, not adjusted to account for changes in the mix of employees from month-to-month. Usually this makes no visible difference to the data, but in April the job losses were disproportionately concentrated in relatively low-wage sectors like leisure and recreation,” Shepherdson wrote.

Wages are likely going down, not going up

The 4.7% growth, he stressed, doesn’t mean that underlying wage growth is rising. In fact, it’s probably falling — something that makes sense given the pay cuts seen thus far during the crisis.

“The opposite story will emerge in the data over the remainder of the year, because unemployment will remain elevated for the foreseeable future, putting downward pressure on wage growth,” Shepherdson said.

While some analysts have suggested ignoring these numbers, others have noted that the misleading information does, in fact, have utility. It stresses who is losing the jobs.

“The average hourly earnings figure jumped to 4.7%, for the month, which indicates that most of the jobs lost were in the lower end of the pay scale,” wrote Charlie Ripley, senior investment strategist at Allianz Investment Management.

For policy makers, investors, and other labor market observers, this is useful information.

Though the spike in hourly earnings may not really be good news, there is a silver lining in “today’s dismal jobs report,” according to MUFG’s Rupkey.

“It is in the realization that the economy cannot possibly get any worse than it is right now,” he wrote.

As Rupkey sees things, joblessness can only get better from here, as states start reopening. Joblessness can only diminish from this point forward as many states start reopening.

“The labor market is a game of musical chairs in every recovery from recession as cash-strapped companies facing less demand for their goods and services are unable to rehire everyone who was laid off in a downturn,” he wrote. “Nevertheless, the skies look brighter here for the economic outlook if only because it cannot get any worse.”

--

Ethan Wolff-Mann is a writer at Yahoo Finance focusing on consumer issues, personal finance, retail, airlines, and more. Follow him on Twitter @ewolffmann.

Why the unemployment rate could be 5 percentage points higher

Frontier Airlines adopts and quickly rescinds $39 to $89 fee for social distancing

Here's a list of CEOs taking pay cuts amid the coronavirus crisis

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube.