money

money Coronavirus fears are creating a mortgage refinancing boom

This article has been updated with latest 30-year fixed mortgage rates and new insight from experts.

As fears over the coronavirus grew, so did the opportunity for homeowners to lock in lower mortgage rates.

The number of mortgage refinance applications jumped 26% during the last week of February week versus the previous one, according to a weekly index from the Mortgage Bankers Association, and was more than triple the volume — up 224% — compared with a year ago.

“I’ve had unprecedented volume come through, with my phone constantly ringing,” said Scott Sheldon, senior loan officer at Sonoma County mortgages. “I have about four times as much volume refinancing.”

Read more: Refinancing mortgages: The full breakdown

The mini refinance boom this week came as Wall Street investors fled stocks in droves and poured money into less risky bonds as concerns over the coronavirus and the global economy mounted.

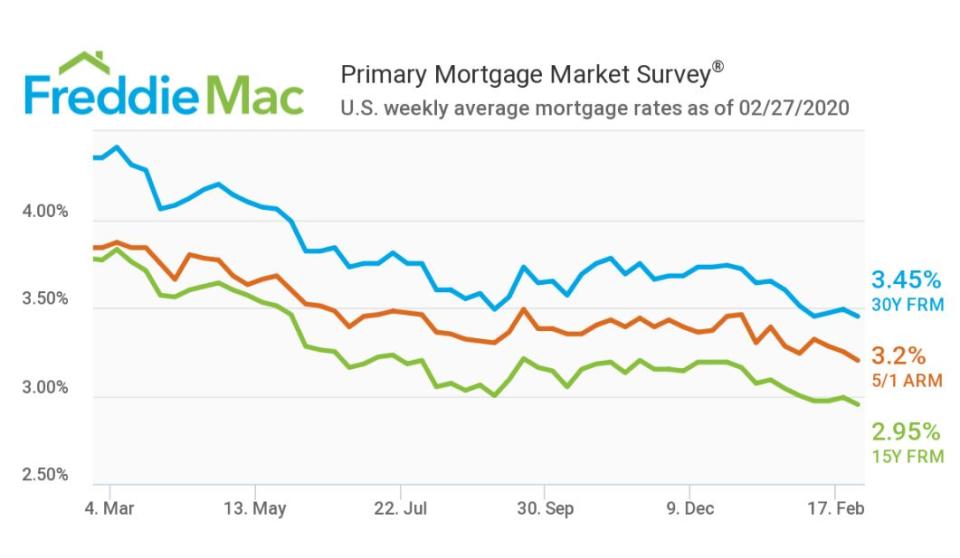

And that uptick may just be the beginning of a refinancing boom. This week, the rate on the 30-year home loan dipped to 3.29%, according to Freddie Mac, the lowest level in 50 years, which could spur more homeowners into action.

“Anybody who has gotten a loan in the latter half of 2018 were likely to save a full percentage point,” said Michael Fratantoni, chief economist at the MBA. “About 80% of households could have lowered their mortgages by half a percentage point.”

Another surge in refinances could be in the offing after a crucial benchmark for fixed interest rates hit an all-time low this week and the Federal Reserve, in an emergency move, slashed a key short-term rate.

More to come?

Rates could fall further.

The yield on the 10-year-Treasury dropped fell below 1% for the first time ever on Tuesday and then carved out another record low on Friday. Historically, fixed mortgage rates tend to follow the yield on the 10-year Treasury.

“But while mortgage rates follow the treasury yield we will see mortgage rates stabilize at 3%,” said Odeta Kushi, deputy chief economist for First American Financial Corporation, a provider of title insurance.

The Federal Reserve also cut its federal funds rate by a half-percent on Tuesday, which affects short-term consumer and business loans.

These cuts will more directly benefit homeowners with adjustable-rate mortgages, or ARMs.

While the Fed’s move doesn’t immediately affect fixed-rate mortgages directly, it sets the tone for a generally lower interest-rate environment.

“The Fed is looking ahead and looking at the risk of a severe economic slowdown and putting in measures that would mitigate this,” Fratantoni said. “We, as long with many others, expect the Fed will cut to even lower rates this year.”

Should you refinance?

If you should refinance it depends on your situation — and not just on rates.

“Someone who is planning on moving in the next couple years shouldn’t refinance,” said John Stearns, senior mortgage loan originator at American Fidelity Mortgage.

Homeowners should also consider closing costs associated with refinancing. These costs can range from 3% to 6% of the mortgage’s value. While the current rate may be lower than yours, it may not be low enough to make the cost of refinancing make sense.

Read more: When to refinance a mortgage

Last, you may want to refinance if you want lower monthly payments. In Sonoma County alone, Sheldon states that buyers on average could have up to $100,000 more in spending power due to lower monthly payments.

“On average,” Sheldon said, “I’m seeing people lower their monthly payments by anywhere from $400 to $600 dollars.”

Dhara is a writer for Yahoo Money and Cashay, a new personal finance website. She can be reached at dhara.singh@yahoofinance.com. Follow her on Twitter @dsinghx.

Read more:

Read more personal finance tips, guides, and news on Cashay.

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, SmartNews, LinkedIn, YouTube, and reddit.