money

money 13 Best Debt Consolidation Loans for Fair Credit

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

A debt consolidation loan is a type of personal loan that lets you combine multiple debts and leaves you with just one loan and one payment to manage. You might also qualify for a lower interest rate, which could help you save money on interest charges and even pay off your loan faster.

While you’ll typically need good to excellent credit to qualify for a debt consolidation loan, there are several lenders that offer debt consolidation loans for fair credit. You can learn about different lenders and see your prequalified personal loan rates when you use Credible.

13 best lenders for debt consolidation with fair credit

If you have fair credit — usually considered to be a credit score between 640 and 699 — you might still qualify for a debt consolidation loan from certain lenders.

Here are Credible’s partner lenders that offer fair credit personal loans for debt consolidation:

Avant

If you have poor or fair credit, Avant could be a good option for a debt consolidation loan. You can borrow $2,000 to $35,000 with repayment terms ranging from two to five years.

Best Egg

Best Egg offers personal loans from $5,000 to $50,000 with loan terms ranging from two to five years. In addition to your credit score, Best Egg also considers more than 1,500 proprietary credit attributes from sources that include external data providers as well as your digital footprint.

This means you might have an easier time qualifying with Best Egg compared to traditional lenders.

Discover

If you’re looking for a longer repayment term on a fair credit personal loan, Discover might be a good choice. You can borrow $2,500 to $35,000 with terms from three to seven years.

Lending Club

LendingClub is one of the few lenders that allow cosigners on personal loans, which could make it a good option if you need a cosigner to qualify. With LendingClub, you can borrow $1,000 to $40,000 with a three- or five-year term.

LendingPoint

LendingPoint specializes in working with borrowers who have near-prime credit — generally meaning credit scores in the upper 500s or 600s. You can borrow $2,000 to $36,500 with terms ranging from two to five years.

LightStream

If you need to consolidate a large amount of debt, LightStream could be a good option. You can borrow $5,000 and $100,000 with repayment terms ranging from two to seven years. If you’re approved, you could have your funds as soon as the same business day.

Marcus

Marcus debt consolidation loans are available from $3,500 to $40,000 with repayment terms from three to six years. Additionally, if you make 12 consecutive on-time payments on a Marcus loan, you can defer one monthly payment interest-free.

OneMain Financial

Unlike many other personal loan lenders, OneMain Financial doesn’t have a minimum required credit score — which means it could be a good option if you have poor or fair credit.

You can borrow $1,500 to $20,000 with terms from two to five years, though keep in mind that larger loan amounts might require collateral.

Payoff

Payoff loans are available for $5,000 to $40,000 and are specifically designed for credit card consolidation. Additionally, Payoff offers free FICO score updates and will work with you on payments if you lose your job.

PenFed

If you only need to consolidate a small amount of debt, PenFed might be a good choice — you can borrow as little as $600 up to $50,000 with terms from one to five years. Keep in mind that you’ll need to join the credit union if you are approved and decide to accept the loan.

Prosper

With Prosper, you can borrow $2,000 to $40,000 with a three- or five-year term. Keep in mind that because Prosper is a peer-to-peer lender, the loan process can take longer compared to other lenders — on average, it takes three to five business days from start to origination if you’re approved.

Universal Credit

Universal Credit offers small personal loans from $1,000 to $20,000 with three- or five-year terms. Also, Universal Credit offers personal loans for bad credit and fair credit — which means you might have an easier time qualifying even if your credit is less than perfect.

Upgrade

Upgrade offers personal loans from $1,000 to $50,000 with terms of two, three, five, or six years. Additionally, Upgrade borrowers have access to free credit monitoring and educational resources that could help you build your credit.

Upstart

If you have little to no credit, Upstart could be a good choice — in addition to your credit, it will consider your education and job history to determine creditworthiness.

How to get a debt consolidation loan with fair credit

If you’re ready to get a debt consolidation loan with fair credit, follow these four steps:

Check your credit. When you apply for a personal loan for debt consolidation, the lender will review your credit to determine your creditworthiness. It’s a good idea to check your credit before you apply to see where you stand. You can use a site like AnnualCreditReport.com to review your credit reports for free. If you find any errors, dispute them with the appropriate credit bureaus to potentially boost your credit score.

Compare lenders and choose a loan option. Be sure to compare as many lenders as you can to find the right loan for you. Consider not only interest rates but also credit requirements, repayment terms, and any fees charged by the lender. Afterward, pick the loan option that best suits your needs.

Complete the application. Once you’ve chosen a lender, you’ll need to fill out a full application and submit any required documentation, such as tax returns or pay stubs.

Get your funds. If you’re approved, the lender will have you sign for the loan so you can get your money. The time to fund for personal loans is usually about one week — though some lenders will fund loans as soon as the same or next business day after approval. You might also have the option to have the funds sent directly to your creditors, depending on the lender.

Do debt consolidation loans hurt your credit score?

Anytime you apply for a new loan, the lender will perform a hard credit check to determine your creditworthiness. This could cause a slight dip in your credit score — though this is usually only temporary, and your score will likely bounce back within a few months.

Tip: A debt consolidation loan could help your credit if you make all of your payments on time. In general, this positive effect on your credit score could outweigh any initial negative impact on your credit score.

If you decide to take out a debt consolidation loan, be sure to also consider how much that loan will cost you over time. This way, you can prepare for any added expenses. You can estimate how much you’ll pay for a loan using a personal loan calculator.

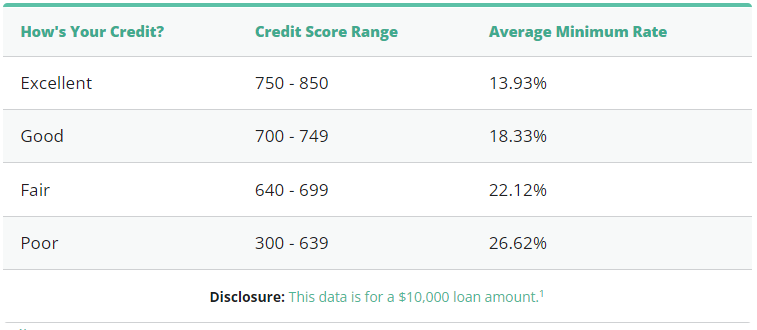

What is a fair credit score?

In general, a fair credit score is considered to be a FICO score between 640 and 699. Here are the credit score ranges you’ll typically come across:

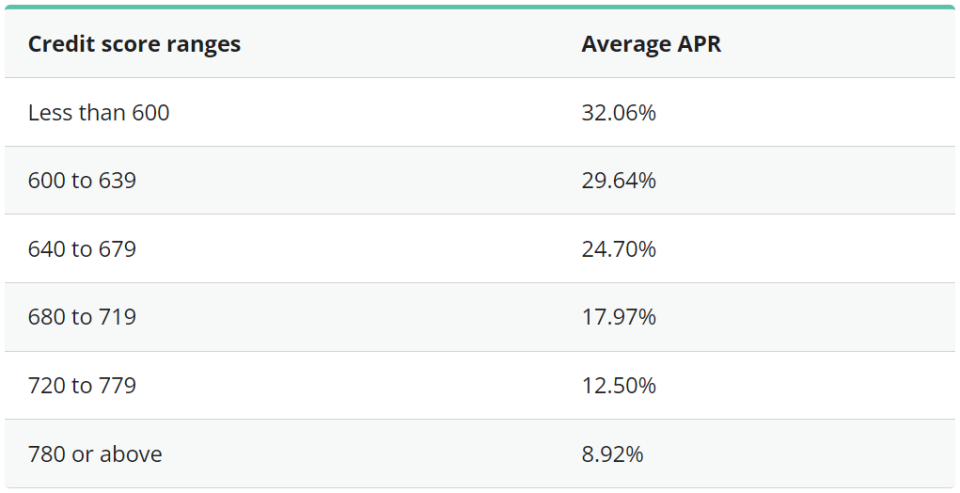

Personal loan interest rates by credit score

Your credit score plays a large role in deciding what interest rate you qualify for, along with your repayment term and the lender itself. In general, the better your credit, the lower the interest rate you’ll likely get — which means you’ll pay less in interest over the life of your loan.

Here are the average personal loan interest rates by credit score offered to borrowers who used Credible to take out a three-year personal loan in December 2021:

How much of a loan can you get with a 600 credit score?

Personal loans typically range from $600 to $100,000, depending on the lender. However, if you’re looking to get a personal loan with a 600 credit score (or lower), keep in mind that your credit score, repayment term, and other factors will likely affect how much you’ll actually be able to borrow.

Tip: If you’re struggling to get approved for a personal loan, applying with a cosigner could improve your chances. While most lenders don’t allow cosigners on personal loans, some do. Having a cosigner might also help you qualify for either a lower interest rate or a higher loan amount — though keep in mind that if you can’t make your payments, your cosigner will be on the hook for repaying the loan.

Before taking out a personal loan for debt consolidation, remember to consider as many lenders as possible to find a loan that works for you. Credible makes this easy — you can compare your prequalified rates from multiple lenders in two minutes.

How to boost your credit score

While you might qualify for a debt consolidation loan with fair credit, these loans often come with higher interest rates compared to good credit loans. If you’d like to get approved for better rates in the future, it could be a good idea to spend some time building your credit.

Here are a few ways to potentially boost your credit score:

Pay all of your bills on time: Payment history makes up the biggest part of your credit score — 35%. Making on-time payments could help you build a positive payment history while improving your credit score.

Pay down credit card balances. Your credit utilization — or the amount of debt you owe compared to your credit limits — makes up 30% of your credit score. Paying down credit cards and other debts could help reduce your credit utilization and boost your score.

Become an authorized user. A simple way to help build credit — especially if you don’t have a credit history yet — is to become an authorized user on a credit card account. This can help build your credit without you even having to use the card.

Raising your credit score could help you save money in the long run on future loans, as you’ll have a better chance of qualifying for lower rates.

For example: Say you had a 600 credit score and took out a $20,000 personal loan with a three-year term. If you qualified for the average 29.26%, you’d end up paying $10,274 in interest over the life of the loan.

But if you were able to boost your score to 680 and got approved for the average 17.96% APR, you’d pay only $6,015 in interest.

About the author: Dori Zinn has been a resident expert in personal finance for nearly a decade. Her writing has appeared in Wirecutter, Quartz, Bankrate, Credit Karma, Huffington Post, and more. She previously worked as a staff writer at Student Loan Hero.

The post 13 Best Debt Consolidation Loans for Fair Credit appeared first on Credible.