money

money 12 Best Personal Loans for Fair Credit

Content provided by Credible. Although we do promote products from our partner lenders who compensate us for our services, all opinions are our own.

This article first appeared on the Credible blog.

You’ll typically need good to excellent credit to qualify for a personal loan. If you have fair credit — usually considered to be a credit score between 640 and 699 — you might have a harder time getting approved. However, there are several lenders that offer personal loans for fair credit.

Keep in mind that the best personal loans for fair credit provide competitive interest rates, a wide selection of loan terms, and inclusive eligibility requirements. With Credible, you can easily compare your prequalified personal loan rates from multiple lenders in minutes.

13 best personal loans for fair credit

Before you take out a personal loan, it’s important to consider as many lenders as possible. This way, you can find the right loan for your situation.

Here are Credible’s partner lenders that offer personal loans for fair credit:

Avant

Avant could be a good choice for borrowers with poor or fair credit. You can borrow $2,000 to $35,000 with repayment terms from two to five years.

Pros

Accepts poor credit scores

Funding as soon as the next business day (if approved by 4:30 p.m. CT on a weekday)

No prepayment penalty

Cons

Not available in Colorado, Iowa, Hawaii, Vermont, Nevada, New York, or West Virginia

Administration fee up to 4.75%

Charges late and dishonored payment fees

Best Egg

With Best Egg, you can borrow $5,000 to $50,000 with repayment terms from two to five years. If you’re approved, you could have your funds within one to three business days after successful verification — which could make it a good option if you need cash quickly.

Pros

Might be able to borrow up to $50,000

Accepts poor credit scores

Fast loan funding

Cons

Not available in Iowa; Vermont; Washington, D.C.; or West Virginia.

0.99% to 5.99% origination fee

Charges late fees

Discover

If you’re looking for a longer repayment term, Discover could be a good choice — you can borrow $2,500 to $33,000 and can pick a term from three to seven years. Just keep in mind that opting for a longer term means you’ll pay more in interest over time.

Pros

Repayment terms up to 7 years

Funding as soon as the next business day after acceptance

If you decide you don’t want the loan, you can return the funds within 30 days and won’t be charged interest

Cons

Minimum credit score is in the upper range of fair credit

Charges late fees

Can’t add a cosigner to the loan

LendingClub

LendingClub personal loans range from $1,000 to $40,000 with three- or five-year repayment terms. You might also get a lower rate if you plan to use a LendingClub personal loan to pay off credit cards or other debt and let LendingClub pay your creditors directly.

Pros

Could get a lower rate if you use your loan to consolidate debt and let LendingClub pay your creditors directly

Accepts poor credit scores

Credit score won’t be affected if you’re denied a loan

Cons

Origination fees from 1% to 6%

Charges late fees

Limited repayment terms (only three or five years)

LendingPoint

LendingPoint specializes in working with borrowers who have near-prime credit — typically meaning a credit score in the upper 500s or 600s. You can borrow $2,000 to $36,500 with repayment terms from two to five years.

Pros

Accepts poor credit scores

Funding as soon as the next business day

Very competitive rates for borrowers with poor or fair credit

Cons

Can only borrow up to $25,000

Origination fees from 0% to 6%

Not available in Nevada or West Virginia

LightStream

If you need to borrow a large amount, LightStream could be a good option — you can borrow $5,000 to $100,000. Most LightStream loans come with terms from two to seven years, but if you’ll be using the loan for home improvements, you could have up to 12 years to repay it.

Pros

Loans up to $100,000

Funding as soon as the same business day

0.50% autopay discount

Cons

Minimum credit score is in the upper range of fair credit

Not available in Rhode Island or Vermont

Doesn’t disclose minimum income requirements

Marcus

Marcus personal loans are available from $3,500 to $40,000 with repayment terms from three to six years. Additionally, if you make 12 consecutive, on-time payments, Marcus will let you defer one monthly payment interest-free.

Pros

No fees

0.25% autopay discount

Can defer one monthly payment interest-free after making 12 consecutive, on-time payments

Cons

Minimum credit score is in the upper range of fair credit

Doesn’t disclose minimum income requirements

Potentially longer funding time compared to some other lenders

OneMain Financial

Unlike many other lenders, OneMain Financial has no minimum required credit score — which means you might have an easier time getting approved even if you have poor or fair credit. In addition to your credit history, OneMain Financial considers your financial history, income, and expenses to determine your creditworthiness.

You can borrow $1,500 to $20,000 with repayment terms from two to five years. Keep in mind that larger loan amounts might require collateral.

Pros

No minimum credit score

Funding as soon as the same day (usually requires a visit to a branch office)

Previous customers might qualify for larger loans

Cons

Loan origination fees vary by state

If approved, you’ll need to visit a branch location to discuss your options

Higher rates compared to other lenders

PenFed

A PenFed personal loan could be a good option if you only need to borrow a small amount — you can borrow as little as $600 up to $50,000 with repayment terms from one to five years. PenFed also charges no fees for its loans.

Pros

Can borrow small loan amounts

No fees

Can use for a variety of purposes

Cons

Minimum credit score is in the upper range of fair credit

Doesn’t disclose minimum income requirements

Must join the credit union if you are approved and decide to accept the loan

Prosper

Prosper offers personal loans from $2,000 to $40,000 with three- or five-year terms. Keep in mind that because Prosper is a peer-to-peer lender, loan funding can sometimes take longer compared to other lenders — on average, the process takes three to five business days from start to origination.

Pros

No prepayment penalty

No minimum income requirement

Can be used for a variety of purposes

Cons

Origination fees from 2.4% to 5%

Not available in Iowa, North Dakota, or West Virginia

Funding could take up to 14 days (though might be as soon as one business day)

Universal Credit

You can borrow $1,000 to $50,000 with Universal Credit and choose a term of three or five years. In addition, Universal Credit will pay off your cards directly if you opt for a credit card payoff loan. You might also get a rate discount.

Pros

Accepts poor or fair credit scores

Free credit monitoring and educational resources

Funding within one day, once approved

Cons

Origination fees from 4.25% to 8%

Higher rates compared to other lenders

Limited information on its website

Upgrade

With Upgrade, you can borrow $1,000 to $50,000 with terms of two, three, five, or six years. Additionally, Upgrade provides free credit monitoring and educational resources that could help be helpful for building your credit.

Pros

Fast approval decisions

Free credit monitoring and educational resources

Funding within a day of clearing necessary verifications

Cons

Origination fees from 2.9% to 8%

Not available in West Virginia

Limited repayment terms (three or five years)

Upstart

In addition to your credit, Upstart will also consider your education and job history to determine creditworthiness — which means you might still qualify even if you have little to no credit history. You can borrow 0$1,000 to $50,000 with Upstart.

Pros

Considers education and job history in addition to credit

No prepayment penalty

Low minimum income requirement ($12,000)

Cons

Origination fees from 0% to 8%

Charges late and returned check fees

Not available in Iowa or West Virginia

Methodology

To find the “best companies,” Credible looked at loan and lender data points from 10 categories to give you a well-rounded perspective on each of our partner lenders. Here’s what we considered:

Interest rates

Repayment terms

Repayment options

Maximum loan amount

Loan funding time

Fees

Discounts

Customer service availability

Whether the minimum credit score is available publicly

Whether consumers could request rates with a soft credit check

Our hope is that this will be a win-win situation for you and us — we only want to get paid if you find a loan that works for you, not by selling your data. This means Credible will only get paid by the lender if you finish the loan process and a loan is disbursed. Additionally, Credible charges you no fees of any kind to compare your loan options.

How to qualify for a loan with fair credit

While eligibility criteria vary between lenders, there are a few common requirements you’ll likely come across, including:

Fair to excellent credit: To get approved for a personal loan, you typically need good to excellent credit — however, there are also several lenders that will work with borrowers who have fair credit. Fair credit usually refers to credit scores from 640 to 699, but you might be able to qualify with a score as low as 580 with certain lenders.

Verifiable income: Lenders want to see that you can afford to repay the loan. Some have minimum income requirements while others don’t — but in either case, you’ll likely need to show proof of income.

Low debt-to-income ratio: Your debt-to-income (DTI) ratio is the amount you owe in debt payments each month compared to your income. Personal loan lenders usually like to see a DTI ratio of 40% or less — though some lenders might make exceptions to this.

Consider applying with a cosigner

If you’re struggling to get approved for a personal loan, consider applying with a creditworthy cosigner to improve your chances. Even if you don’t need a cosigner to qualify, having one could get you a lower interest rate than you’d get on your own.

Keep in mind that not all lenders allow cosigners on personal loans, but some do.

How to apply for a fair-credit loan

If you’re ready to apply for a fair-credit personal loan, follow these four steps:

Research and compare lenders. Be sure to compare as many personal loan lenders as possible to find the right loan for your needs. Consider not only interest rates but also repayment terms, any fees charged by the lender, and credit requirements.

Pick your loan option. After you’ve compared lenders, choose the loan option that works best for you.

Complete the application. Once you’ve picked a loan option, you’ll need to fill out a full application and submit any required documentation, such as tax returns or pay stubs.

Get your funds. If you’re approved, the lender will have you sign for the loan so the money can be released to you. The time to fund for a personal loan is usually about one week — though some lenders will fund loans as soon as the same or next business day after approval.

How to choose a fair credit lender

While personal loan lenders might appear similar on the surface, it’s important to do your research and compare your options from as many lenders as possible. This way, you can find a loan that best suits your needs.

Here are some important points to keep in mind as you weigh your options:

Interest rate: Your interest rate will play a major role in determining your overall loan cost. Several factors will influence the rates you’re offered, including your credit score and repayment term. In general, the higher your credit score, the better your rate will be. Applying with a cosigner might also help you get a lower interest rate.

Loan amount: You can typically borrow $600 up to $100,000 (or more) with a personal loan. Be sure to borrow only what you need to keep your repayment costs manageable.

Repayment term: Personal loan repayment terms usually range from one to seven years, depending on the lender. While choosing a longer term might get you a lower monthly payment, it’s usually best to choose the shortest term you can afford to keep your interest costs as low as possible. Additionally, many lenders offer better rates to borrowers who opt for shorter terms.

Fees: Some lenders charge fees on personal loans (such as origination fees or late fees), which could increase your overall loan cost. Note that if you take out a loan with one of Credible’s partner lenders, you won’t have to worry about prepayment penalties.

Keep in mind: Credible only partners with vetted, trustworthy lenders. If you choose to take out a loan with one of Credible’s partners, you can rest assured that you’ll be working with a quality lender.

How to improve your fair credit score

While you might still be able to get a personal loan with bad credit or fair credit, these loans usually have higher interest rates compared to good credit loans.

However, there are a few ways to potentially improve your credit score so you can qualify for better rates in the future, such as:

Make all of your payments on time. Your payment history makes up the largest part of your FICO credit score. Paying all of your bills on time can help build a positive payment history and possibly boost your credit score.

Pay down credit card balances. The next largest part of your credit score is your credit utilization — which is how much you owe on revolving credit lines compared to your limits. If you can pay down your balances to lower your credit utilization — such as by paying more than the minimum on your balances — you could help build your credit.

Consolidate your debt. Another way to potentially lower your credit utilization is by using a personal loan to consolidate credit cards and other debt. Personal loans usually come with lower interest rates than credit cards, which means taking out a debt consolidation loan might save you money on interest charges, too.

Get credit for other bills. You can have payments for utilities, phones, subscriptions, and more reported to the credit bureaus by using a service like Experian Boost. This can quickly help boost your credit score.

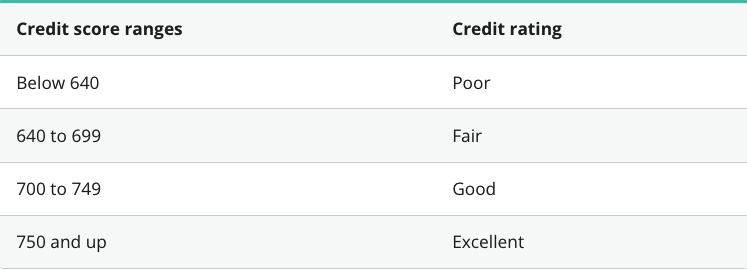

What does a fair credit score mean?

Your credit score is a three-digit number that lenders use to determine how likely you are to repay a loan. Credit scores can range from poor to excellent — here’s how these ranges break down:

Generally, the better your credit score, the more likely lenders will be willing to work with you. If you have a fair credit score (in the range of 640 to 699), your credit isn’t necessarily bad, but it could make it harder to qualify for a loan. Fair credit loans also tend to come with higher interest rates compared to good credit loans.

Remember that your credit score is made up of five factors — payment history, credit utilization, credit history length, credit mix, and new credit. This means that there could be multiple reasons why you have a fair credit score — for example, maybe you’ve:

Missed some payments on your bills

Racked up high credit balances

Applied for several new loans in a short period of time

How much will a fair credit personal loan cost?

How much a personal loan will cost mainly depends on your credit and the interest rate you qualify for. In general, the better your credit score, the lower your interest rate — and the less you’ll pay over the life of the loan.

For example: Borrowers who used Credible to get a three-year personal loan in May 2021 and who had credit scores between 640 and 679 received an average personal loan interest rate of 24.57%.

If you took out a $10,000 personal loan with a three-year term and this 24.57% rate, you’d end up paying $6,348 in interest over the life of the loan. But if you were able to improve your credit and qualify for a lower interest rate of 18%, you’d pay only $4,522 in interest.

Before taking out a personal loan, it’s important to consider how much that loan will cost you. This way, you can be prepared for any added expenses. You can estimate how much you’ll pay for a loan using Credible’s personal loan calculator.

About the author: Angela Brown is a student loan, personal finance, and real estate authority and a contributor to Credible. Her work has appeared in Fox Business, LendingTree, FinanceBuzz, and Yahoo Finance.

The post 12 Best Personal Loans for Fair Credit appeared first on Credible.